Paying the usual monthly bills, car loans, student loans, home loans, credit card balances … saving for retirement can be a challenge when you have so many other competing priorities. And because retirement seems far, far away in the distant future, it can be easy to put off saving for it until someday. But setting aside even a small amount every month starting now can pay bigger rewards than you might think.

Best Ways to Save

Many employers offer a retirement plan, either a 401(k) or 403(b), as part of a benefits package. With these kinds of plans, you simply choose how much you want to contribute from each paycheck toward your retirement. That amount is automatically deducted and invested in the plan. Some employers offer a match, usually 50% of what you contribute, up to a certain limit, depending on the company. As an example, if you contribute 6% of your paycheck, your employer may contribute up to 3%. Voila! You’re now saving almost 10% of your paycheck!

If your employer does offer a matching contribution, make sure you contribute enough to qualify for it—otherwise you’re missing out on free money. For example, if you contribute $100 per two-week pay period, and your employer matches that at 50%, you’re effectively saving $300 a month ($150 x 2), but it’s only costing you $200. And when you get a raise, increase your retirement savings accordingly. You won’t even miss it.

Another advantage of these kinds of employer-sponsored retirement plans is that your contributions are tax deductible. If you earn an above-average salary, retirement plan contributions effectively reduce your taxable income during your peak earning years. You only pay tax when you make withdrawals from the plan, which is why these investments are considered tax deferred. Your contributions and the returns they earn grow tax-free. As of 2021, 401(k) annual contribution limits are $19,500 for those under 50 years old. If you’re 50 or over, you can make an additional catch-up contribution of $6,500, for a total of $26,000.

Even if your employer offers a retirement plan, you may still want to open an individual IRA, especially a Roth IRA for those just starting out. Although contributions are limited to $6,000 a year ($7,000 for those 50 and over), these plans are completely self-directed, meaning that you get to choose from a larger universe of investments. Traditional IRAs are tax deductible and tax deferred, just like 401(k)s. Contributions to a Roth IRA are not tax deductible; however, their earnings and all future withdrawals are tax-free. Investments in a 401(k) or traditional IRA can also be converted or transferred into a Roth IRA, but must be held for at least five years before withdrawal to be exempt from taxes.

Why is it important to start saving early? The magic of time.

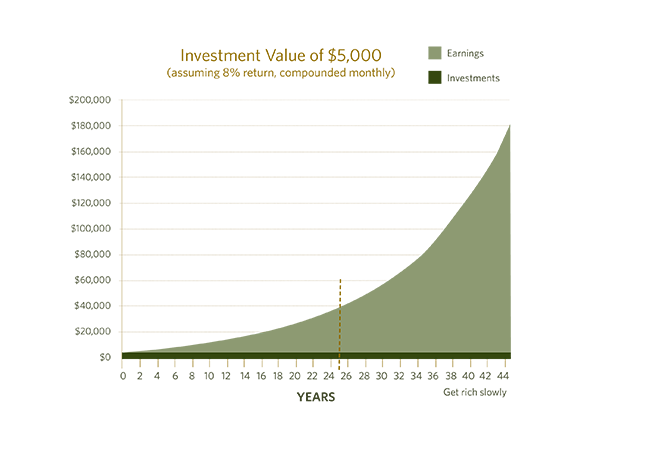

In a nutshell, the power of compound interest makes it important to start saving early. The longer your retirement savings have to grow, the less you need to invest. Starting early, at 25 or 30, means you can save a smaller amount every month and end up with more money in retirement than someone who saves a larger amount but waits until 40 or 45 to start. The graph below shows the growth of a single, one-time investment of $5,000.

The light green area shows how much money compound interest adds to that original $5,000 investment. After 25 years, it’s grown to just under $40,000—not too shabby. But after 45 years, $5,000 has grown to $180,000! That could be your account.

Time is truly the magic ingredient when saving for retirement. Imagine what your results when you are ready to stop working if you added to your retirement savings every month.

Please see additional IMPORTANT DISCLOSURE INFORMATION.